In the first part of this series, I compared becoming a new parent to nurturing relationships with new customers (and also managing their payments). The intent was for entrepreneurs to take 5 minutes every now and then to reflect on one element of their businesses to help them grow. In this article, I will focus on a growing pain for many small businesses—that being debt management (particularly Creditors, otherwise known as Accounts Payable).

Did you pack enough nappies?

The first trip out with a newborn is an adventure, and planning for the trip is exceptionally important. Will it be too cold? Perhaps too hot? How many change of clothes should a pack? Do I have wet wipes? Pacifiers? A changing mat? The dozen or so creams I need? And, most importantly, did I pack enough nappies?

Most entrepreneurs start their business journey off with a great idea, a burning passion, however, not much planning or forethought. For example; the trendy building closest to home seems like the perfect place to set up shop. Your mom’s best friend from school gives you the best discount for supplies. Your old school friend works in the local bank and can help get you a great loan.

Some of these might seem perfect or even too good to be true for your business. And in some cases, they may be your only option. But in all cases, what is in your control, are the terms of these agreements and management of them. These landlords, suppliers and banks are the people you will owe most of your money to (i.e. your creditors).

A little planning here can make a big difference towards the long-term success of your business. A few points to consider:

- What is your ideal payback period? 30, 60, 90 days – this is ALWAYS negotiable.

- Will there be bulk-order discounts?

- What are the interest / penalties on late payments?

- What are the service level agreements (SLAs) in terms of quality and timing of delivery?

- Outline the clawbacks and refunds when SLAs are breached.

- Are there any non-compete clauses? i.e. potentially prevent competitors from an advantageous supplier.

Invest in (baby) monitors

We had a scare with our newborn, just one week after coming home from the hospital. His temperature spiked, fever set in, and we subsequently spent the next week in ICU as he (and the antibiotics) fought off an infection. All is fine now, but it could have been a lot worse if we were not attentive or monitoring changes in him. So, although the above planning and contract negotiation is important, you should also be monitoring these contracts with your creditors.

Businesses and the economy change constantly, and as a result, what was once a good deal may become a poor one in a short period of time. But given that you are busy and trying to grow your own business, how do you monitor these numerous contracts?

Here are a few tips:

- Review at least one creditor per month. Take time to see if you can get a better deal with that creditor, or if there is a better option in market. Starting with the latter will give you leverage to negotiate with the existing creditor.

- Where it makes business sense, consolidate creditors. One payment (rather than multiple) is easier to manage and possibly could get you better terms for having multiple contracts, e.g. mortgage and loans from the same bank, or bulk discounts from suppliers.

- Invest in a simple, easy to use reporting solution and technology.

The latter is probably the most important as it enables the first two. Doing things manually takes time. A piece of paper with your brainstorming notes on is not really usable for the next month. Microsoft Excel is probably the easiest and most familiar to use, and it can help you analyse your creditors to a certain extent. Many businesses use Excel in fact, but most find that the constant updating and potential for human error becomes a problem as the business scales.

Sage Intelligence is a reporting solution that understands this, and therefore combines the use of your accounting system and Excel. Basically, you set up an Excel template once, and each month when opened through Sage Intelligence, the template is populated with the latest data stored on your accounting system (as well as data from previous periods). It’s a build once and use many model.

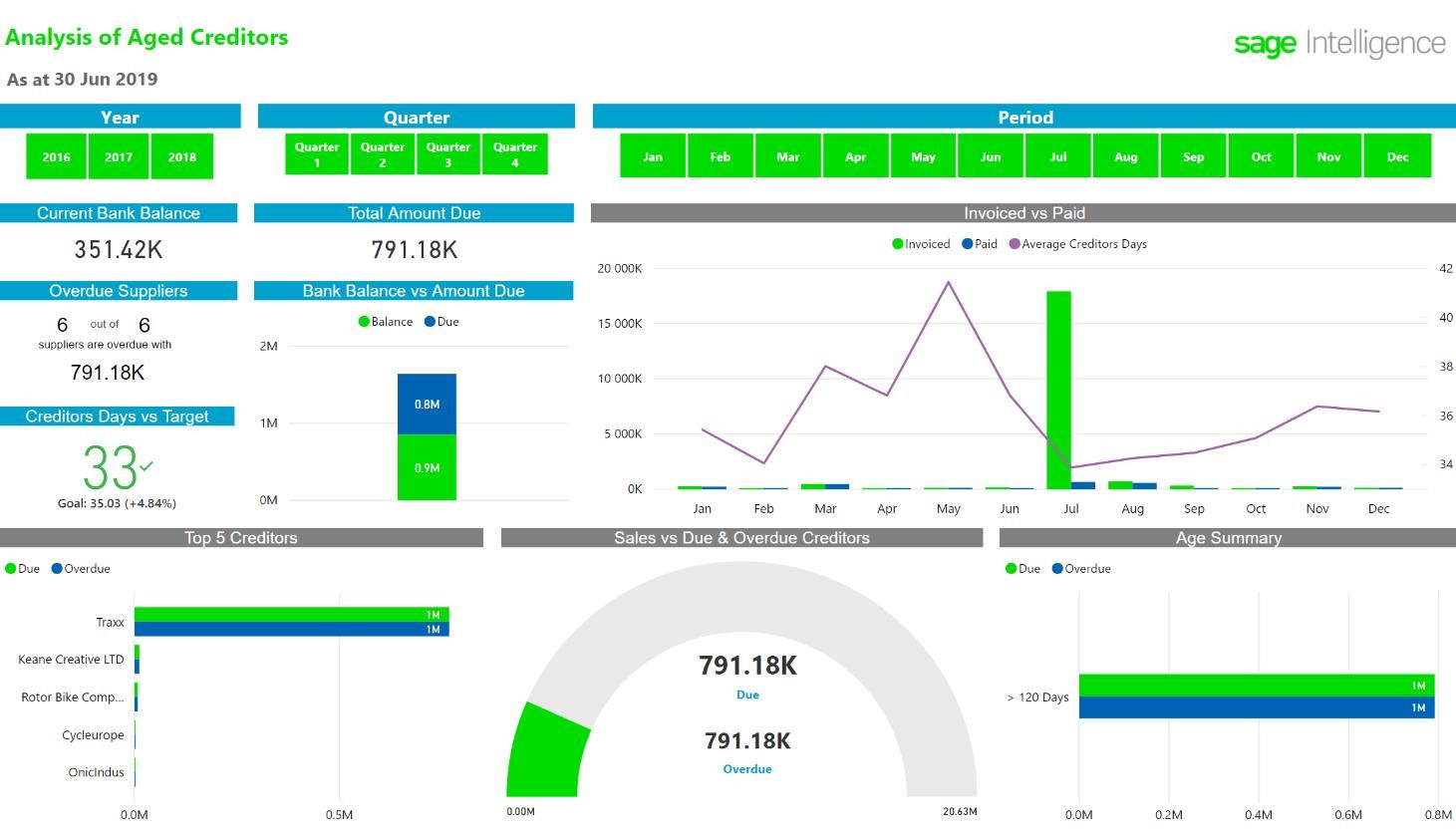

However, having the data at your fingertips is only useful when you get insights from what you are seeing. This is where visualisations come in, whether it’s a simple Microsoft Excel chart that shows how much you owe your creditors and how long their balance is outstanding, or a more complex visualisation like the below Sage Intelligence powered, Microsoft Power BI report.

Using the above, you can quickly see who you owe most of your debt to, when it needs to be paid, and whether you are overdue or not. It also shows trends and a history of your creditor management. The report also brings in the information you need to manage this debt, for example; your bank balance, the size of the debt versus your sales, and when you seem to occur the most debt, i.e. just before big sales season. Taking a few minutes every month to look at the above could greatly help you manage your debt.

P.S. Debt is scary and can be detrimental to your business. However, most good businesses use debt to their advantage. In bigger companies, it is an indicator used by financial analysts to determine if a business is being managed successfully through their use of leverage. The premise is ROI from debt usage > debt financing. So, when you next fight for that 5% interest rate on your loan, make sure you make at least a 6% return on the investment (e.g. profit mark-up on emergency order goods bought with the loan).